New yacht or none-paid VAT (EU or to be imported )

Yacht to be bought by a VAT-registered maritime company from a vendor located outside the state of the future home port;

Yacht to be registered under a statute authorizing her operation by chartering;

In Spain, the yacht has to be crewed when chartered according to the Spanish charter licence.

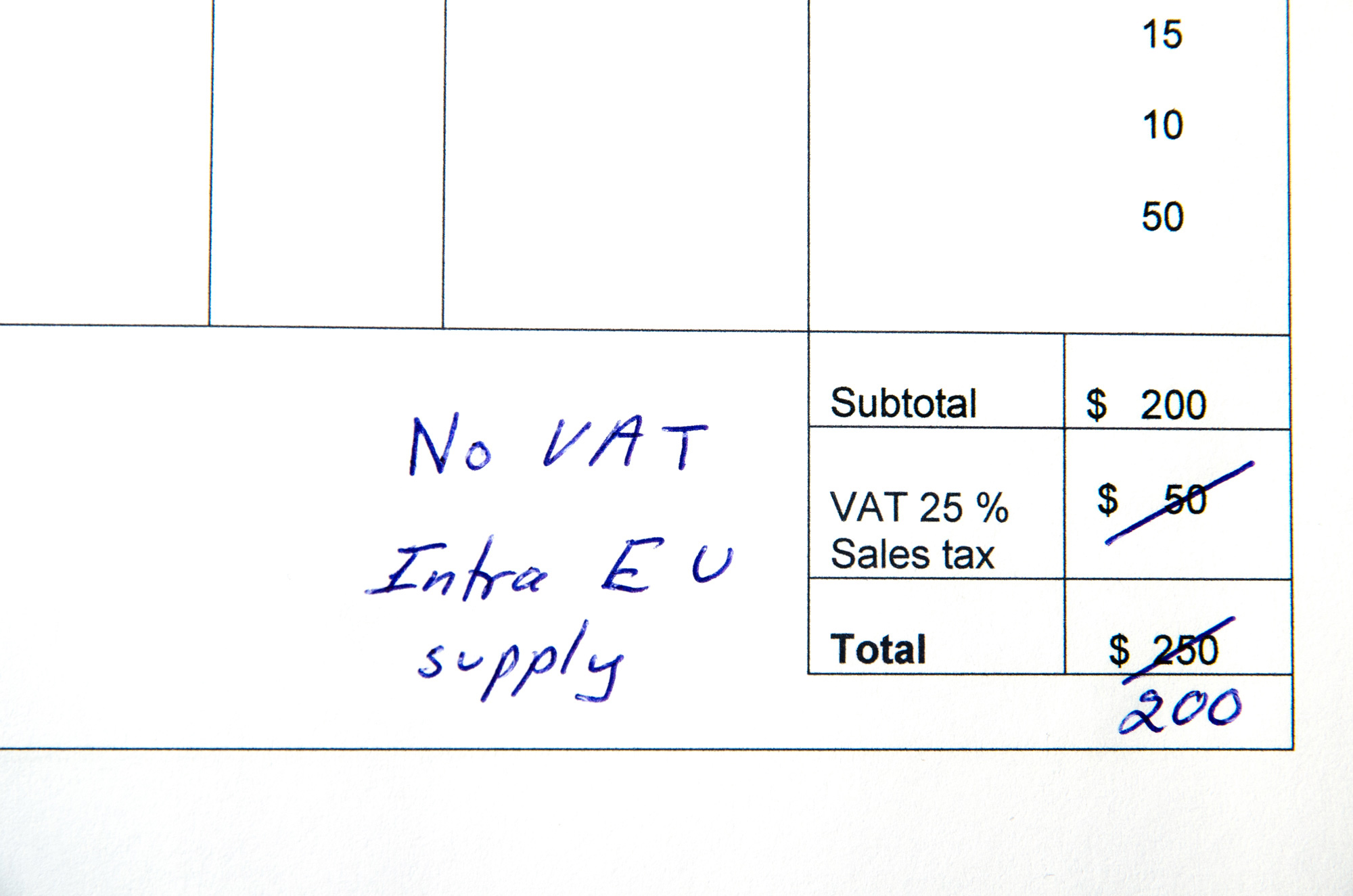

Regarding VAT, the intra-Community acquisition of a yacht qualifies as reversed charge operation. It still remains the condition that the yacht has to be operated by chartering.

The owner is welcomed to be the charterer, this under the condition to pay the charter rate at market’s arms length.

Onward Supply Relief (OSR): Should the Yacht be imported to the EU, we will apply the Onward Supply Relief (OSR) to the future home port and handle the operation as B2B intra-Community (reversed charge) acquisition.